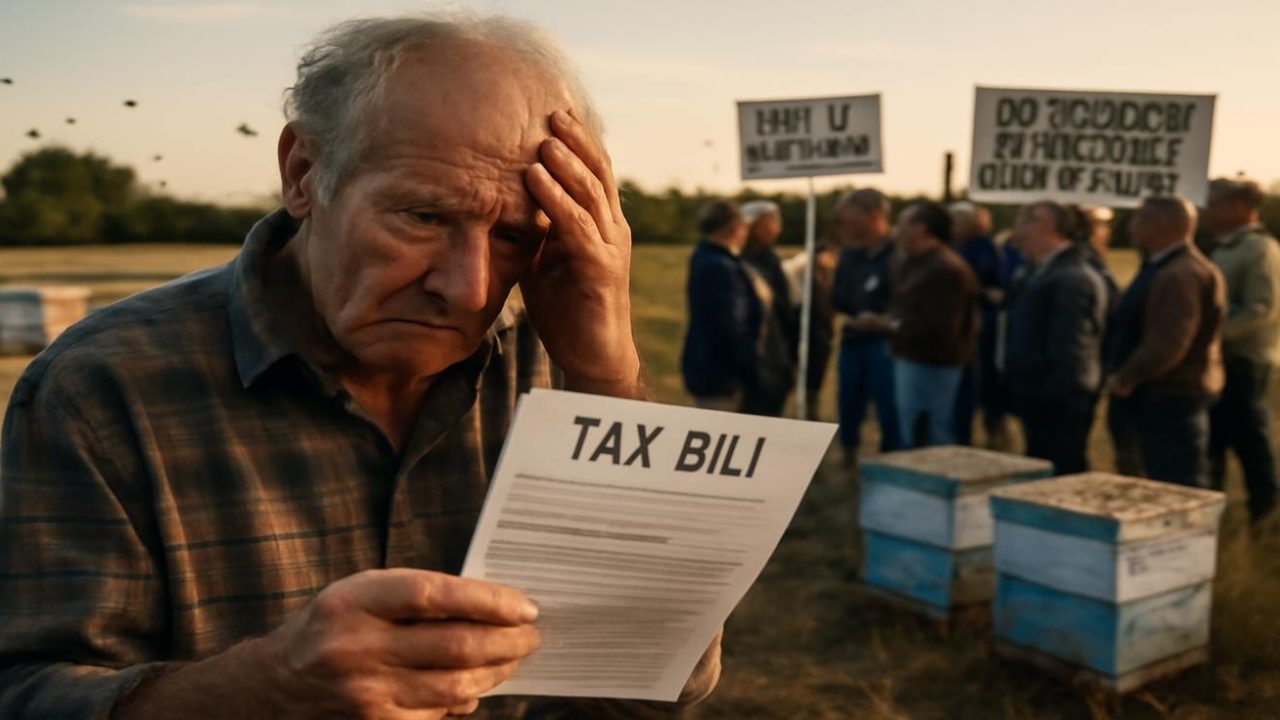

A 72-year-old Texas retiree’s simple act of kindness—allowing a beekeeper to place hives on his 12-acre property for free—has resulted in a crushing tax bill that threatens to cost him his family farm. The case highlights a brutal irony in agricultural tax law: sometimes doing good can trigger devastating financial consequences.

Henry’s story began when he retired from his local feed store and decided to help a beekeeper by providing free land for bee colonies. What seemed like a win-win arrangement—bees would pollinate his wildflowers while the beekeeper got free space—turned into a bureaucratic nightmare that could cost him everything.

The financial blow came in the form of a thick government envelope containing an agricultural tax adjustment. Years of rollback taxes, penalties, and interest had accumulated into a bill that Henry describes as being “like another house” in terms of cost.

How Agricultural Tax Exemptions Actually Work

Henry’s land had been taxed under Texas’s agricultural valuation system for decades. This isn’t actually a tax exemption—it’s a significant discount for landowners who actively use their property for qualifying agricultural purposes like grazing cattle, growing hay, raising goats, or keeping bees.

After Henry’s wife Anne passed away, she had always handled the paperwork. Henry sold off their cattle because the work was too demanding and the market was poor. However, he didn’t realize that maintaining the agricultural tax status required continuous compliance and documentation.

The problem arose when Henry stopped running cattle without officially registering another qualifying agricultural use. When he allowed the beekeeper to set up hives without payments or formal paperwork, the property fell into a regulatory gray area—not quite farming, not quite residential.

Agricultural valuations operate as year-by-year contracts rather than permanent designations. When the county determined that Henry’s land was no longer in compliance, they applied rollback taxes retroactively for multiple years, plus penalties and interest.

The Bureaucratic Logic Behind the Financial Storm

From the government’s perspective, the tax adjustment follows established rules designed to prevent abuse. The rollback system exists to recover lost tax revenue when land changes from agricultural to other uses, preventing wealthy landowners from gaming the system with minimal agricultural activities.

| Tax Status | Requirements | Consequences of Non-Compliance |

|---|---|---|

| Agricultural Valuation | Active qualifying agricultural use | Rollback taxes, penalties, interest |

| Market Value | No agricultural requirements | Higher annual tax burden |

| Gray Area | Unclear or undocumented use | Risk of retroactive reclassification |

The state’s logic is straightforward: if land stops being used for agriculture, it should be taxed like any other property. The rollback provision ensures that landowners can’t benefit from agricultural tax rates while not actually farming.

However, Henry’s situation reveals the harsh reality of how these rules can punish genuine agricultural activity when proper documentation is missing. His arrangement with the beekeeper was providing a legitimate agricultural service, but without formal contracts or payment records, the county couldn’t verify it met their requirements.

Why This Case Matters Beyond One Farm

Henry’s predicament exposes a fundamental conflict between community-minded generosity and bureaucratic requirements. He was genuinely supporting agricultural activity by hosting bees, which benefit both local ecosystems and food production through pollination.

The case raises questions about whether current agricultural tax systems adequately account for informal but legitimate farming arrangements. Many small-scale agricultural activities operate through handshake agreements and community cooperation rather than formal business contracts.

For landowners across Texas and other states with similar agricultural tax programs, Henry’s experience serves as a cautionary tale about the importance of understanding compliance requirements. Even well-intentioned agricultural use can trigger devastating tax consequences without proper documentation.

The situation also highlights how agricultural tax law can inadvertently discourage environmental stewardship. Beekeeping provides crucial pollination services and supports biodiversity, yet informal arrangements to support such activities can create tax liability rather than recognition.

The Broader Implications for Agricultural Communities

Henry’s story reflects a larger tension in rural communities where informal cooperation has traditionally been the norm. Many agricultural arrangements operate on trust and mutual benefit rather than formal contracts, but tax systems increasingly require detailed documentation.

The rollback tax system, while designed to prevent abuse, can create situations where legitimate agricultural activity is penalized due to paperwork failures rather than actual non-compliance. This creates particular hardship for elderly or retired farmers who may not understand evolving bureaucratic requirements.

For beekeepers and other agricultural service providers, cases like Henry’s could make it more difficult to find land for their operations. Property owners may become reluctant to enter informal arrangements if they risk triggering tax penalties.

The financial impact extends beyond individual cases. When family farms are lost due to tax burdens, it affects local agricultural capacity and community stability. Henry’s 12-acre property represents not just personal loss but the erosion of rural agricultural infrastructure.

What This Means for Other Landowners

Property owners with agricultural tax valuations need to understand that these benefits require active compliance and documentation. Simply having agricultural activity on the land isn’t sufficient—the use must be properly registered and documented according to local requirements.

Anyone considering allowing agricultural use of their property should consult with tax professionals and county assessors before making arrangements. Even generous, environmentally beneficial activities like hosting beehives can trigger tax consequences without proper planning.

The case also demonstrates the importance of understanding rollback tax provisions. When agricultural tax status is lost, the financial consequences can extend back multiple years, creating bills that far exceed annual tax obligations.

For communities that rely on informal agricultural cooperation, Henry’s experience suggests a need for better education about tax compliance requirements and potentially policy reforms that better accommodate community-based agricultural arrangements.

Frequently Asked Questions

What exactly triggered Henry’s tax bill?

His land lost agricultural tax status when he stopped running cattle without properly documenting the beekeeping activity as a qualifying agricultural use.

How do agricultural tax valuations work?

They provide reduced tax rates for land actively used for qualifying agricultural purposes, but require year-by-year compliance and documentation.

What are rollback taxes?

These are retroactive tax adjustments that recover the difference between agricultural and market value taxation when land loses its agricultural status, often including penalties and interest.

Could Henry have avoided this problem?

Yes, by properly documenting the beekeeping arrangement and ensuring it met county requirements for agricultural tax status before allowing the hives on his property.

Do other states have similar tax systems?

Many states offer agricultural tax programs with similar compliance requirements and rollback provisions for non-qualifying land use.

What happens to Henry’s farm now?

The source material indicates he faces a crushing tax bill but does not specify the final outcome or whether he can keep the property.

Leave a Comment