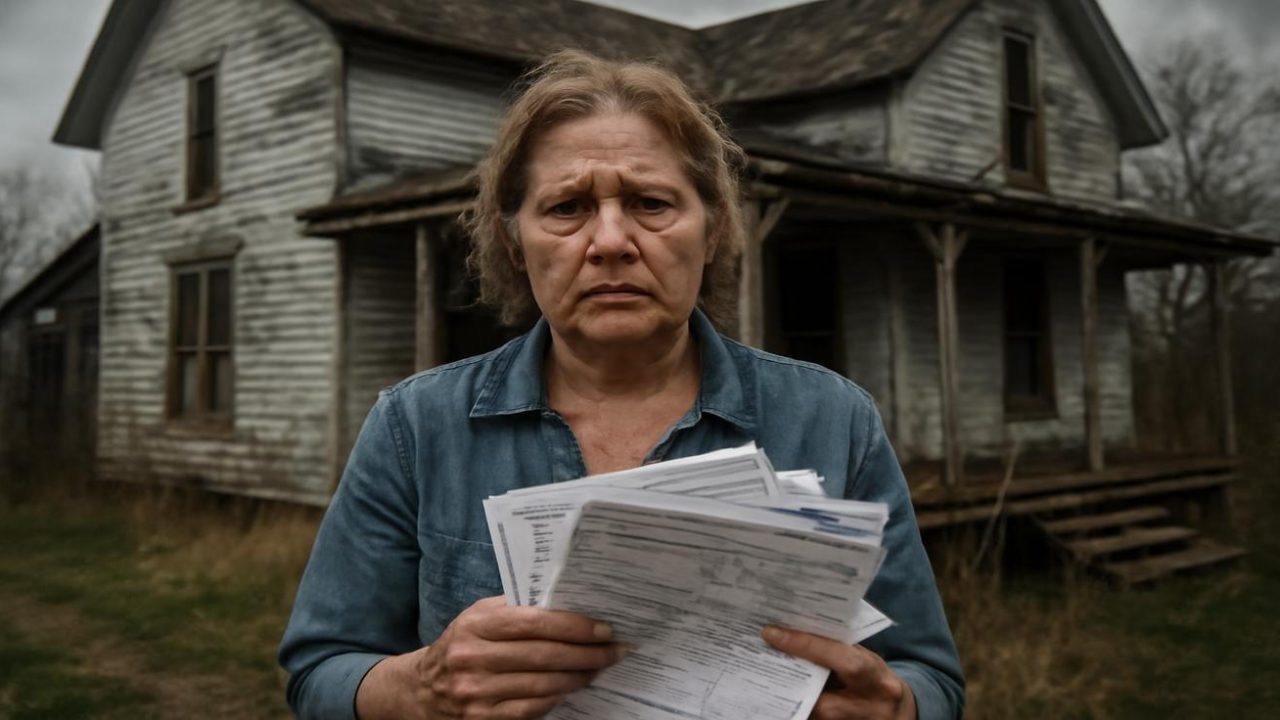

A daughter who moved back to her family’s crumbling farmhouse to care for her dying father received a devastating surprise seven months after his death: a tax reclassification notice demanding a decade of backdated property taxes. The county had labeled her a “commercial landlord” despite never collecting rent from anyone.

The case highlights a growing problem across rural America, where adult children caring for aging parents in family homes face unexpected tax consequences that can destroy both finances and family relationships. What should be recognized as sacrifice is instead being punished as profit.

The letter arrived with the first snow, containing numbers with more zeros than the caregiver’s bank account had ever seen. After nearly ten years of paying heating bills, patching roofs, and giving up career advancement to provide end-of-life care, she discovered the government considered her property use “commercial rental.”

How Caregiving Became “Commercial Activity”

The farmhouse sat on a wind-scoured rise at the edge of town, where neat subdivisions gave way to patchy fields and stands of maple. Built by her grandparents and passed to her parents, the tired home featured avocado-green cabinets, complaining floorboards, and a septic system that groaned under pressure.

When her mother died suddenly on an August morning, the choice arrived like a storm front. She could stay in the city with her rented apartment and office job, or drive home to help her father, whose lungs were failing and who had repeatedly said he wanted to die in the house, not “in some room with linoleum floors and plastic curtains.”

She chose family over career. After moving back, she properly re-registered her address, changed her mailing details, driver’s license, and voter registration. Every form confirmed the same story: this was her primary residence, reclassified by insurance as “owner-occupied.”

The property had been mortgage-free for years. She never collected rent, never advertised rooms, never operated any kind of business. Yet somehow, caring for her dying father triggered a tax reclassification that would haunt her years later.

The Hidden Costs of Family Caregiving

Life in the farmhouse shrank to the rhythm of medication schedules, doctor’s appointments, and the soft hiss of an oxygen machine. The land around them didn’t care about paperwork – summers brought riots of milkweed and bees, while winters sucked color from everything but the red barn and blue enamel mug she kept beside the kettle.

The financial sacrifice was immediate and measurable. Career advancement stopped. City weekends disappeared. The steady hum of a predictable life gave way to uncertainty, but she had accepted these costs as part of caring for family.

What she hadn’t anticipated was the government’s interpretation of her living situation. The tax office’s logic appeared to be that any adult child living in a parent’s home – even as a caregiver – constituted a rental arrangement subject to commercial property taxes.

| Aspect | Before Reclassification | After Reclassification |

|---|---|---|

| Property Status | Owner-occupied residence | Commercial rental property |

| Tax Rate | Residential rate | Commercial rate (significantly higher) |

| Retroactive Period | N/A | 10 years of back taxes |

| Rental Income | $0 collected | Assumed “undeclared income” |

When Sacrifice Meets Bureaucracy

The reclassification notice arrived with the weight of official authority, printed on thick paper with the county tax office logo. The “COMMERCIAL – RENTAL” designation appeared alongside demands for “outstanding back taxes due for ten-year period” based on “undeclared income” that never existed.

The farmhouse still smelled like her parents’ laundry detergent and woodsmoke, not like a commercial enterprise. Shingles lifted in high winds, one bathroom sink only ran hot when coaxed properly, and the whole structure showed its age in ways that would make any legitimate landlord cringe.

Yet bureaucratic logic had transformed this family tragedy into a business transaction. The daughter who had given up promotions and city life to provide end-of-life care was now facing financial ruin for her decision to prioritize family over career.

The Broader Pattern of Punishing Care

This case reflects deeper tensions in how society values caregiving versus commercial activity. While the tax code offers numerous incentives for business investment and property development, it provides few protections for families navigating end-of-life care in multi-generational homes.

The timing makes the situation particularly cruel. The tax bill arrived seven months after her father’s death, when grief was still fresh and the financial strain of medical expenses was already overwhelming. Rather than recognizing the sacrifice involved in family caregiving, the system treated it as a profit-making venture.

Rural communities face particular challenges as aging populations require care in family homes that may not fit standard residential classifications. Adult children who move back to help elderly parents often find themselves caught between family obligations and bureaucratic interpretations that assume financial rather than emotional motivations.

What This Means for Other Families

The implications extend far beyond one family’s tax bill. As more adults face decisions about caring for aging parents, the specter of retroactive tax penalties adds another layer of complexity to already difficult choices.

Families considering multi-generational living arrangements need to understand how local tax authorities might interpret their situations. What seems like a straightforward family decision can trigger commercial property classifications with significant financial consequences.

The case also highlights the need for clearer guidelines about when family caregiving arrangements cross the line into commercial activity. Current interpretations appear to vary widely, leaving families vulnerable to unexpected reclassifications years after making caregiving decisions.

Legal experts suggest that families document the non-commercial nature of caregiving arrangements, maintain clear records of who pays household expenses, and consult with tax professionals before making major living arrangement changes.

Frequently Asked Questions

What triggered the commercial property reclassification?

The tax office appears to have interpreted an adult daughter living in her parents’ home while providing care as a rental arrangement, despite no rent being collected.

Can families appeal these types of reclassifications?

The source material doesn’t specify appeal processes, but the case suggests families may face significant bureaucratic challenges in reversing such decisions.

How common are retroactive tax penalties for family caregiving?

The source doesn’t provide statistics on frequency, but indicates this reflects broader tensions between family obligations and tax code interpretations.

What documentation might protect families in similar situations?

While not specified in this case, maintaining clear records of the non-commercial nature of caregiving arrangements and who pays household expenses could be important.

How long was the retroactive tax period in this case?

The tax office demanded back taxes for a ten-year period, covering the entire time the daughter lived in the family home as a caregiver.

Was any actual rental income involved?

No, the daughter never collected rent from anyone, yet the tax office assumed “undeclared income” from the living arrangement.

Leave a Comment