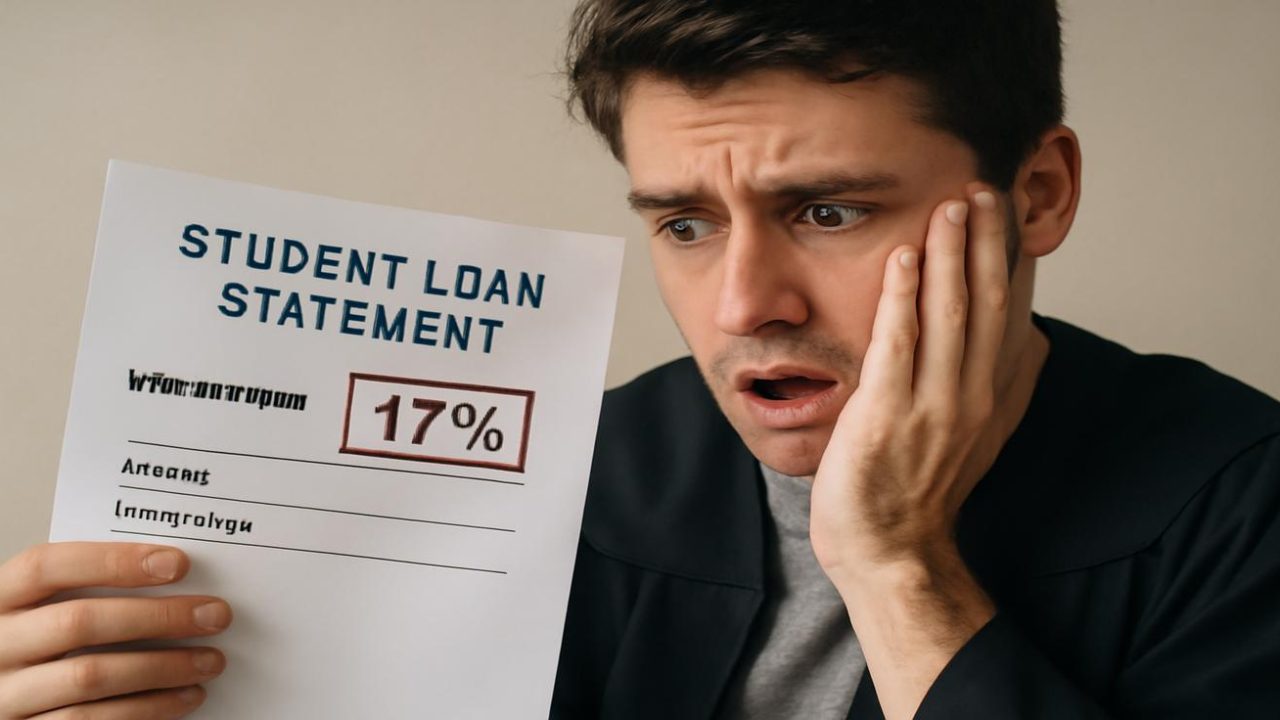

A college graduate making regular $412.36 monthly payments on her student loans discovered she was facing a 17% interest rate — turning what she believed was steady progress into a financial trap that kept her debt growing despite years of on-time payments.

The shocking reality hit when an email notification revealed the true cost of her education financing. Like millions of other borrowers, she had been focused on making minimum payments without fully understanding how high interest rates were undermining her efforts to become debt-free.

Her story highlights a widespread problem in student lending that affects borrowers nationwide, where complex loan terms and buried interest rate details can transform manageable monthly payments into decades-long debt cycles.

How Student Loan Interest Rates Create Hidden Traps

The graduate’s experience reveals how student loan systems can mislead borrowers about their true financial obligations. Despite making consistent monthly payments since graduation, her loan balance wasn’t shrinking as expected because the 17% interest rate was consuming most of each payment.

This situation typically develops when borrowers focus solely on meeting minimum payment requirements without examining how much of each payment goes toward principal versus interest. At a 17% annual percentage rate, the majority of early payments serve interest charges rather than reducing the actual debt.

Financial aid offices often present loans as “manageable investments” during the enrollment process, emphasizing monthly payment amounts while downplaying long-term interest costs. Students and families, particularly first-generation college attendees, may lack the financial literacy to fully evaluate these complex loan agreements.

The graduate in question signed her loan documents at age 18, trusting guidance counselors and financial aid officers who assured her the loans were “standard” and wouldn’t require attention until after graduation. Her parents, having never attended college themselves, were reluctant to ask detailed questions about terms they didn’t understand.

The Real Cost of High-Interest Student Loans

High interest rates can dramatically extend repayment periods and total costs for student borrowers. The difference between a typical federal loan rate and a 17% private loan rate can add tens of thousands of dollars to the final repayment amount.

Consider how interest rates affect monthly payments and total costs:

| Loan Amount | Interest Rate | Monthly Payment | Total Interest Paid | Payoff Time |

|---|---|---|---|---|

| $30,000 | 5% (Federal) | $318 | $8,200 | 10 years |

| $30,000 | 17% (Private) | $412 | $47,000 | 25+ years |

The graduate’s $412.36 monthly payment seemed reasonable compared to her nonprofit salary, but the 17% rate meant she was paying more in interest than many borrowers pay toward their entire loan balance each month.

Private student loans, unlike federal loans, often carry variable interest rates that can increase over time. Borrowers may sign agreements with promotional rates that later adjust upward, sometimes reaching the high teens for borrowers with limited credit history.

Warning Signs Every Student Loan Borrower Should Know

Several red flags can indicate that loan payments aren’t making meaningful progress toward debt elimination:

- Monthly statements show minimal principal reduction despite consistent payments

- The loan balance remains nearly unchanged after a year of payments

- Interest charges consume 70% or more of each monthly payment

- The total amount owed continues increasing despite regular payments

- Loan servicers offer only minimum payment options without principal-focused alternatives

Many borrowers, like the graduate featured in this case, make automatic payments without carefully reviewing monthly statements. This autopilot approach can mask the reality that minimum payments on high-interest loans often barely cover interest charges.

The psychological impact of discovering these loan traps can be devastating. Borrowers who believed they were making responsible financial progress suddenly realize their debt situation is far worse than anticipated, leading to feelings of betrayal by the educational financing system.

Why First-Generation Students Face Higher Risks

First-generation college students are particularly vulnerable to predatory lending practices in educational financing. Without family members who have navigated the student loan process, these students often lack advocates who can identify problematic loan terms.

The graduate’s parents trusted the college’s financial aid guidance without questioning interest rates or long-term costs. This deference to institutional authority is common among families where college attendance represents a significant achievement and departure from previous generations’ experiences.

Private lenders often target students at schools with limited federal aid availability, presenting private loans as necessary supplements to complete degree programs. Students facing immediate enrollment deadlines may accept unfavorable terms rather than delay their education.

The complexity of loan documents, written in technical language with crucial details buried in fine print, makes it difficult for inexperienced borrowers to understand their true obligations. Interest rate information may be disclosed in multiple locations using different calculation methods.

Steps Borrowers Can Take to Address High-Interest Student Loans

Borrowers trapped in high-interest student loans have several potential options for improving their situations:

- Loan consolidation or refinancing through lower-rate lenders

- Income-driven repayment plans for federal loans

- Extra principal payments to reduce interest accumulation

- Employer-sponsored loan assistance programs

- Public service loan forgiveness for eligible careers

However, borrowers should carefully evaluate any changes to their loan terms, as refinancing federal loans into private loans eliminates federal protections like income-driven repayment and forgiveness programs.

The graduate’s situation demonstrates why financial literacy education should be mandatory before students sign loan agreements. Understanding compound interest, payment allocation, and long-term costs could help future borrowers make more informed decisions about educational financing.

Frequently Asked Questions

How can student loan borrowers find out their actual interest rates?

Check your monthly loan statements or log into your loan servicer’s website to view current interest rates for each loan.

Is a 17% interest rate legal for student loans?

Yes, private student loan interest rates can legally reach the high teens, especially for borrowers with limited credit history.

Can borrowers challenge interest rates they didn’t fully understand when signing?

Legal challenges are generally unsuccessful unless fraud or deceptive practices can be proven in the loan origination process.

What’s the difference between federal and private student loan interest rates?

Federal loans typically have fixed rates in the single digits, while private loans can have variable rates reaching 15-18% or higher.

Should borrowers always make more than minimum payments on student loans?

Extra payments toward principal can significantly reduce total interest costs, especially on high-rate loans, but borrowers should ensure they have emergency savings first.

How do automatic payments affect borrowers’ awareness of their loan terms?

Automatic payments can create a false sense of progress if borrowers don’t regularly review statements showing how payments are allocated between interest and principal.

Leave a Comment